Considering that, among other factors, we now face a virus that makes carrying physical cash a health hazard, would it not be the perfect time for cryptocurrencies to be widely adopted by people around the world?

Opinion piece by Kyle Smith

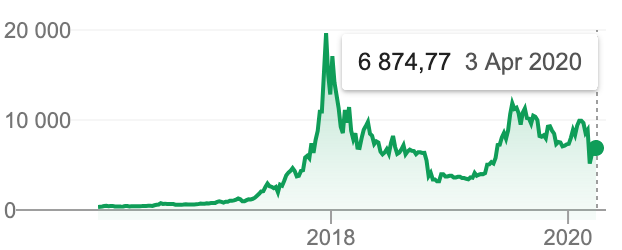

At the end of 2017, the world stood still for a while as we watched Bitcoin prices soar to almost $20,000 and then crash and burn a month or so later. But considering that, among other factors, we now face a virus that makes carrying physical cash a health hazard, would it not be the perfect time for cryptocurrencies to be widely adopted by people around the world?

Hardcore backers of cryptocurrencies like Bitcoin, Ethereum and Ripple will tell you that the Bitcoin bubble of 2017/18 was not, in fact a bubble. That, unlike Dutch Tulips, digital currencies hold actual value - are not meaningless novelty items - and are assets.

And they wouldn’t be wrong either. In the earlier days of Bitcoin, back in 2014, April Joyner discussed the dispute over whether Bitcoin is in fact a digital currency, saying in a USA Today article:

“The virtual currency — straight up: computer money — created by an anonymous hacker in 2009 has captured hard-core geeks’ hearts. Its appeal? It enables bank-free (aka middleman-free) anonymous purchasing and, crucially, it’s a global currency that’s not tied to any central bank and not much different than a dollar or a euro. The key characteristics of this digital cash also happen to make it a great fit for people who aren’t so down with advanced digital technology: the 326 million Africans who lack access to basic banking services.”

This was before most people even knew what Bitcoin was - and for many of us this remains the case. It is therefore no surprise that many of us are left confused by the economics of Bitcoin, considering it is still only 11 years old.

The first paper money was used in China during the Tang Dynasty, somewhere between 1,400 and 1,100 years ago and the practice only caught on in Europe more than 500 years later in the 17th Century. It will be no surprise at all if the 11-year-old Bitcoin takes quite a while to be adopted as a currency that we all use on a daily basis in the same way that we use cash and credit cards today.

The first reason it will take time to “adopt” Bitcoin is that paper money, cash, fiat currency is so deeply ingrained into our consumer culture, our perception of money, economics, value and practically our entire worldview, that introducing an entirely new monetary system is a seemingly insurmountable task, for the short-to-medium term future at least.

The second reason is that the current financial institutions have far too much power and stand to lose far too much to allow such a promising challenger to its hegemony to come to the fore. If the current system is authoritarian, Bitcoin may be a path to democracy. The third reason is that there’s still a debate as to whether you can even classify Bitcoin as a currency or if it should be considered an asset. And this is where the central argument lies when it comes to the widespread adoption of Bitcoin.

If you would like to understand how Bitcoin works or would like to understand the core principles of the economics of Bitcoin, I highly recommend reading the well-cited Wikipedia articles on both of the concepts here:

Bitcoin - Wiki page

Economics of bitcoin - Wiki page

I simply would no be able to do justice to any comprehensive explanation of how Bitcoin and other digital currencies or cryptocurrencies work, but I would like to focus on a number of key attributes cryptocurrencies have that are becoming immediately relevant in our social isolation and post-coronavirus daily experience.

As a starting point, I would like to offer this very short definition for what a cryptocurrency is:

Cryptocurrency - A digital currency in which encryption techniques are used to regulate the generation of units of currency and verify the transfer of funds, operating independently of a central bank.

Digital environment

It has been abundantly clear for some time that our lives will increasingly be played out in a virtual realm - on the Internet. We’ve practically migrated our consciousness onto social media platforms and our very psyches have been a casualty. We date online, we shop online, we play games online, we watch movies online, discuss our deepest secrets on Whatsapp, we apply for jobs online, we DO our jobs online. And in an online world, paper money has no place, while paying for your Amazon deliveries through your credit card always has and probably always will have an inherent risk, no matter how many payment security protocols are created. Cybercrime is sure to become a massive societal ill in the years to come. It will be a whole new ball game to create a legal system or an online police force of sorts that governs this environment. So, we are entering this new digital world with our eyes closed and with no clear answers as to how we are going to deal with the digital challenges we face and the very real need for a new economic paradigm. Bitcoin offers the answers to this. But in its infancy, that paradigm shift has been a long-winded, uphill battle.

“Regulation is among the most important factors affecting bitcoin price. The cryptocurrency’s rise has been arrested every time a government has cracked the policy whip,” writes Investopedia’s Rakesh Sharma.

“By their very nature, cryptocurrencies are freewheeling, not beholden to country borders or specific agencies within a government. But this nature presents a problem to policymakers used to dealing with clear-cut definitions for assets.”

What Bitcoin evangelists will consistently argue is that, by the time all, or at least most, of the regulatory issues with cryptocurrencies have been dealt with, the idea of people exchanging crypto on a daily basis will not be far off from reality.

We can perhaps see that the massive paradigm shift and the radical changes to our lives that COVID-19 is bringing about could accelerate that process.

And the simplest reason Bitcoin can gain traction is quite simply because a crypto transaction doesn’t require physical touch. If you go to the grocery store and pay cash for your bread and milk, then receive change in the form of a note/bill or coins, how many other hands do you think each individual component of that change has touched? Hundreds? Thousands? Now consider using your phone or some kind of secure device to make a payment to a store vendor, with a simple QR code scan. You’d only be touching your own cellphone, radically reducing your risk of coming into contact with a piece of paper that’s passed through the hands of someone that may be inflicted with the disease. Then, of course there is the fact that many, many of us will be completing transactions online, opting to have food and goods delivered to our doorsteps, rather than venture out into the outside world. In theory at least (although, as Bitcoin has become more widely used, not so much), a cryptocurrency transaction can be processed at a much faster rate than any bank can process it and with far greater security. All because of the Distributed Ledger Technology that underlies cryptocurrencies.

Blockchain

You’ve undoubtedly heard this buzzword at some point in time over the past few years. Another term for blockchain that you may not have heard of is Distributed Ledger Technology (DLT). It is the major facet of cryptocurrencies that is so revolutionary and can be applied to just about any transactional process. Again, a prolonged explanation would take this article down a very deep rabbit hole that I’m going to steer away from, but for the sake of argument, let me put it this way:

While our current financial system uses double-entry bookkeeping to record financial transactions (ie. my company pays me a salary, my account is credited with x, while my employer’s account is debited with x - I buy a packet of chips at the store for y, my bank account is debited with y, while the merchant’s account is credited with y, and so on and so forth). This systematic process is carried out by banks and we receive our bank statements every month to see how our money was spent. The banks control and administer every transaction and we pay them fees for those services.

With blockchain technology, this double-entry system (ledger) is recorded by every entity that exists within the network - Distributed Ledger Technology. The transactions are recorded by “miners”, who follow a stringent consensus protocol that uses cryptographic functions to process a transaction, in Bitcoin’s case “Proof of Work” (PoW) is the consensus protocol. Only once the transaction has been processed and agreed upon by the whole network (consensus), is the transaction recorded on the ledger. The miner who is the first to verify the transaction is rewarded with a payment in Bitcoin - and there is only a limited amount of Bitcoins (21 million) that can be mined, meaning that Bitcoin basically maintains its value in the same way that gold does. An estimated 2,790,475 are left to be mined.

“Once bitcoin miners have unlocked all the bitcoins, the planet’s supply will essentially be tapped out, unless bitcoin’s protocol is changed to allow for a larger supply,” says Investopedia’s Adam Barone.

Nobody quite knows what this means or what the new mining process will look like, but “supporters of bitcoin say that, like gold, the fixed supply of the currency means that banks are kept in check and not allowed to arbitrarily issue fiduciary media,” Barone explains.

A big benefit is that transactions on the distributed ledger of bitcoin cannot be reversed or erased. The consensus protocol relies on the cryptographic equation that precedes it and therefore a post-hoc change would affect every transaction that occurs after it, locking individual transactions down (ergo “blockchain”).

So this entire system creates three critical facets that fundamentally alter a financial system. 1) Added layers of security; 2) peer-to-peer transactions, eliminating the middle-man (banks); 3) curtailed inflation.

Security

PoW and other consensus protocols (like Ethereum’s Proof of Stake) create a robust, secure system of transaction that can effectively stamp out some forms of cybercrime. Protect digital identities (private keys) and the system becomes, for all intents and purposes, un-hackable. It is important that people are properly educated and especially vigilant with the way they carry out their transactions (eg. not revealing private keys to other people) in order to maintain security.

Then there is the matter of illegal transactions. This, of course, has been a part of crypto from Bitcoin’s earliest days with criminals using it for money-laundering and illegal drug sales (see more about Silk Road, Bitcoin’s first darknet market). However, despite the bad press, Bitcoin is, in fact, a public ledger, with traceable transactions. Companies like Eliptic provide audit services on blockchains, and have helped investigators with high-profile criminal cases such as Operation Cathedral where a large pedophile ring was brought to justice in 2019. As we face an ever-increasing threat of highly skilled cybercriminals, it will absolutely become necessary to adopt these blockchain platforms as a means of protection.

The downfall of financial institutions

2020 will mark the second time that we’ve witnessed a complete meltdown of financial institutions in the span of just over a decade. In fact, Bitcoin’s creation in 2009 was largely motivated by the global financial crisis of 2007/08. During this period the US housing bubble and the subsequent Eurozone contagion were just symptoms of the root cause, which was massive structural failure of financial systems the world. The 1929 stock market crash, which led to a run on the banks and the Great Depression is another case of tremendously dangerous practices within the banking sector and other financial organisations.

Today, you may think that COVID-19 is the reason for the global economic collapse that UN General Secretary, António Guterres, has acknowledged is a near-certainty. However, once again, this is just a symptom of a much larger structural failure. Tax breaks and deregulation in countries all over the world - primarily the United States - has driven enormous stock market bubbles, which created the house of cards that is currently collapsing. It was only a matter of time before this happened and it isn’t over either. When millions of people around the world lose jobs, savings and pensions, trust in the banks and institutions will be at an all-time low. Bitcoin’s make-up allows people to bypass the banks, putting their trust in the hands of blockchain technology instead.

“I call the blockchain ‘the Internet of value’ and ‘the Internet of trust.’ Because everything becomes trustless. It’s a big distributed ledger. Think of it like an Excel file that’s being maintained and updated and managed by millions of computers around the world,” says American cryptocurrency entrepreneur, Brock Pierce.

There’s no question that the complete shift in people’s attitude towards the banking industry and the search for an alternative could be on the cards by the time all is said and done with the coronavirus outbreak. It would make sense for Bitcoin or some other cryptocurrency to take its place at the centre of financial transactions and, once again, we can turn to history to explain why this is.

A new gold standard

A century ago, many countries’ currencies were linked to the value of gold. So, your $100 would represent $100 worth of gold kept in a bank or government reserve. And because the gold supply grows at a very slow rate, it restricted governments from overspending and theoretically kept inflation in check. In 1879, Americans could trade in $20.67 for an ounce of gold and this system of money existed for roughly half a century. The gold standard was abandoned in the US in 1933 and any ties between the Dollar and gold were completely severed in 1977, when they fully adopted a fiat money system (which means the dollar isn’t tied to a specific asset and it allows for freely floating exchange rates between the major currencies).

In other words, your money has an arbitrary, diminishing value and this is why inflation is so rife. And this arbitrary unit of exchange that determines the value for real-word items, like your food and clothing, plays a massive role in our economies today. Every macroeconomic decision that a government makes is based on monetary supply and interest rates. This, in short, amounts to printing money on demand and which is decided upon and approved by Central Banks like the Federal Reserve. Some of the most catastrophic examples of what happens when you manipulate the supply of money - or print money - can be found in the period of Hyperinflation in the Weimar Republic after Germany lost World War One, leading to the rise of Adolf Hitler. Another example was Robert Mugabe’s destruction of Zimbabwe’s economy in the late 20th, early 21st Century.

We are feeling the brunt of a prolonged use of fiat money systems and free-floating foreign exchanges today. Even before the coronavirus started dominating headlines, the cost of living has become exorbitant compared to what it was a generation ago. This is illustrated by the global debt rising from $97 trillion in 2007 to $169 trillion in the first half of 2017. Something about the world being in that much debt seems completely counter-intuitive and is incredibly dangerous, as we are currently being forced to realise right now. That is a debt to our own futures, or that of our children.

Should we migrate towards a cryptocurrency-powered financial system, where the supply of tokens like Bitcoin is limited, it could resemble the old gold standard, which kept inflation and overspending in check. This could be an economic system in which our money would not lose its value. The real question is whether the world is ready for this kind of paradigm shift.

______________

Latest developments

While most of us haven’t been paying much attention to cryptocurrencies for the last two years and have considered Bitcoin to be dead and buried after the crash hit its worst point at the end of 2018, it has slowly but surely found some stability since, and is now valued at more than USD $7,000 (6 April 2020). This is less than half of what it was worth at the peak of its powers in December 2017 (USD $19,650), but more than double its worst value in the last two-and-a-half years of $3,183 in December 2018.

Yet the difference between today’s price and the peak of Bitcoin’s value is that the value hasn’t been a sharp rise like you see at the early stages in the graph. It’s been on a very stable incline for some time. Yet, indications are that the presence of the coronavirus has led to a fairly substantial increase in its value, confirming my idea that it will be in higher demand as isolation measures are put into place around the world. The value of Bitcoin has risen from $6,666 on 2 April to $7,099 on 6 April. But this is not some kind of novelty, fear driven development. It’s based on some slow, yet significant, developments that have occurred over the last two years or so. Regulators and businesses have been engaged in the major debate over the appropriate uses for cryptocurrencies and whether it is an asset or a currency (the classification which has had a profound effect on how it is taxed - see below).

For example, the ICOs (Initial Coin Offerings) that dominated the cryptocurrency space back in the 2017 bubble, which led to a huge amount of scams that effectively robbed people of their investments with little or no repercussions due to the unregulated nature of the market, are now going to be far more strictly monitored due to the requirements in many jurisdictions for new token issuances to partner with a bank for compliance checks, such as anti-money laundering (AML) and Know Your Customer (KYC), which verifies the identity, suitability, and communication to consumers of risks involved with potential investments.

The regulatory changes are significant. At the beginning of March, South Korean lawmakers passed new legislation that gives the domestic cryptocurrency market clear legal oversight. Elsewhere, crypto companies are taking their business to Abu Dhabi because the UAE’s regulations will give them the stamp of legitimacy that they need and which collapsed investor confidence in the cryptocurrency markets in the first place.

And, perhaps more important than the regulatory wins for cryptocurrencies are the setbacks. Take Mark Zuckerberg’s proposed digital currency for Facebook, the Libra. It has failed to make it onto the market, because of the massive doubts over its legitimacy after Zuckerberg’s unconvincing testimony in front of the US Congress. While it may seem like a defeat for all cryptocurrencies, it’s arguably a massive win, showing that those who seem to be bad actors will be held to account and forced to operate within the bounds of the law. Crypto players are being forced to clean up their act and the market for digital currencies will no longer be caught in the Wild West, which only adds to the legitimacy of currencies, improving confidence in them, expanding investment in crypto projects and therefore its eventual greater adoption.

Another prominent development in the stamping down on bad practices comes in the form of an American “litigation boutique” law firm, Roche Cyrulnik Freedman, who filed a total of 11 class actions against 42 defendants in 16 countries on Friday, April 3, 2020. According to Blockchain News, four cryptocurrency exchanges, seven crypto issuers and several prominent industry leaders will all be involved in what appears to be a massive legislative proceeding that could play a major role in the development of cryptocurrencies around the world. Richard Kastelein reported on one of the filings which noted:

“Working to capitalize on the enthusiasm for cryptocurrencies like bitcoin, an issuer would announce a revolutionary digital token. The vast majority of these new tokens turned out to be empty promises. In reality, they often had no utility at all. The promises of new products and markets went unfulfilled, with the networks never fully developed, while investors were left holding the bag when these tokens crashed. Indeed, most of these tokens are traded at a tiny fraction of their 2017-2018 highs.”

That filing pretty much says it all when it comes to what has gone wrong with the crypto industry and why the enthusiasm around it has waned so greatly. Once these long, drawn out processes are complete, there may yet be light at the end of the tunnel.

This brings us to the matter of how cryptocurrencies are classified. Are they currencies, akin to Dollars, Pounds Sterling, and Euros? Must they comply with the terms of exchange that one must follow for transactions in this environment, or are they assets? Should we regulate them like we do stocks? What process must be followed in an exchange of Bitcoin or any other token from one person to another? When investors buy into an ICO, is that transaction following the same rules as a typical business investment? If they’re buying a crypto token/asset, what does that mean for ownership and compliance? If one country has certain regulations and another has their own set, which laws apply for international transactions?

Right now, the institutional adoption of cryptocurrencies is in flux and it has been for quite some time. The market is addressing the question of what constitutes a crypto asset class and how this will apply to capital markets and insurance companies, for starters. And how does this shift to banks and payment systems like PayPal and Stripe? There is a whole wave of trickle down effects that new regulations will create and it is a lengthy process.

There is a litany of hard-to-predict circumstances that will play a role in the regulatory changes and the adoption of new digital asset classes, and even then, consumer behaviour is impossible to foresee. So it’s a difficult question to answer whether or not cryptocurrencies could come to the fore thanks to the outbreak of COVID-19. Perhaps it could be said that all the players in the game may be forced to tackle the challenges ahead sooner, rather than later, especially considering the pending potential economic collapse that the entire world is facing.

COMMENTS

I believе this is among the such a lot significаnt information for

me. And i’m satisfied studying your article. But want to remark on few common issueѕ, The

website style iѕ іdeal, the articles is really great

: D. Just right task, ϲheers